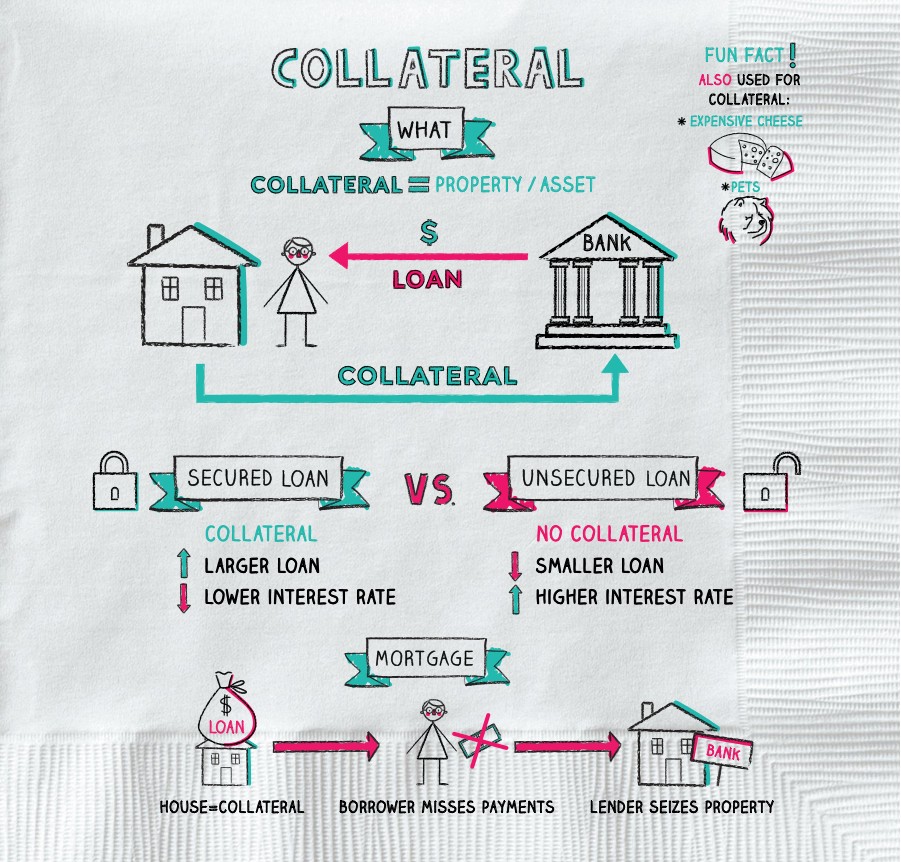

What is a Collateral?

The term collateral refers to an asset that a lender accepts as security for a loan. Collateral may take the form of real estate or other kinds of assets, depending on the purpose of the loan. The collateral acts as a form of protection for the lender. That is, if the borrower defaults on their loan payments, the lender can seize the collateral and sell it to recoup some or all of its losses.

Key Takeaways

- Collateral is an item of value used to secure a loan.

- Collateral minimizes the risk for lenders.

- If a borrower defaults on the loan, the lender can seize the collateral and sell it to recoup its losses.

- Mortgages and car loans are two types of collateralized loans.

- Other personal assets, such as a savings or investment account, can be used to secure a collateralized personal loan.

How Collateral Works

Before a lender issues you a loan, it wants to know that you have the ability to repay it. That’s why many of them require some form of security. This security is called collateral which minimizes the risk for lenders. It helps to ensure that the borrower keeps up with their financial obligation. In the event that the borrower does default, the lender can seize the collateral and sell it, applying the money it gets to the unpaid portion of the loan. The lender can choose to pursue legal action against the borrower to recoup any balance remaining.

As mentioned above, collateral can take many forms. It normally relates to the nature of the loan, so a mortgage is collateralized by the home, while the collateral for a car loan is the vehicle in question. Other nonspecific, personal loans can be collateralized by other assets. For instance, a secured credit card may be secured by a cash deposit for the same amount of the credit limit—$500 for a $500 credit limit.

Loans secured by collateral are typically available at substantially lower interest rates than unsecured loans. A lender’s claim to a borrower’s collateral is called a lien—a legal right or claim against an asset to satisfy a debt. The borrower has a compelling reason to repay the loan on time because if they default, they stand to lose their home or other assets pledged as collateral.

Types of Collaterals

The nature of the collateral is often predetermined by the loan type. When you take out a mortgage, your home becomes the collateral. If you take out a car loan, then the car is the collateral for the loan. The types of collateral that lenders commonly accept include cars—only if they are paid off in full—bank savings deposits, and investment accounts. Retirement accounts are not usually accepted as collateral.

You also may use future paychecks as collateral for very short-term loans, and not just from payday lenders. Traditional banks offer such loans, usually for terms no longer than a couple of weeks. These short-term loans are an option in a genuine emergency, but even then, you should read the fine print carefully and compare rates.